5 Key Points: Your Guide to the OBBBA Tax Changes

- Temporary SALT Cap Relief with a Catch: The State and Local Tax (SALT) deduction cap is temporarily raised to $40,000 until 2029, but this benefit is aggressively phased down for those with an adjusted gross income (AGI) over $500,000, making strategic tax timing crucial.

- Federal Estate Tax Is Effectively Eliminated for Most: With the federal estate and gift tax exemption permanently raised to an inflation-adjusted $15 million per person, estate planning for most high-earners now shifts from tax avoidance to maximizing the "step-up in basis" for heirs.

- A Revolution in Private Investment (QSBS): The Qualified Small Business Stock (QSBS) exclusion is dramatically enhanced with a new tiered holding period (starting at 3 years for a 50% exclusion) and a higher $15 million gain limit, making angel and venture investing significantly more tax-advantaged.

- Charitable Giving Strategy Has Changed: A new 0.5% of AGI "floor" on charitable deductions makes "bunching" contributions into a Donor-Advised Fund (DAF) a far more effective strategy than making smaller, annual gifts.

- Education Funding is Overhauled: 529 plans are now more flexible, covering K-12 expenses and career credentials, while the termination of the Graduate PLUS loan program makes it essential for families to proactively save for high-cost degrees.

High-earning families are once again in the crosshairs of the most major tax changes coming out of Washington since 2017. The "One Big Beautiful Bill Act" (OBBBA), signed into law on July 4, 2025 will affect almost all tax payers, mostly in a positive way compared to sunsetting of current tax laws which was planned to happen at the end of this year.

The bill is controversial in some circles due to its potential impacts on deficits, renewable energy, and healthcare but this article will only focus on the financial impact of high earning households and there are many.

So, what exactly is this sweeping new law? Simply put, the OBBBA makes many of the popular provisions from the 2017 Tax Cuts and Jobs Act (TCJA) permanent while dramatically enhancing others and introducing entirely new concepts. The bill did nothing to create a simpler tax code, instead it added more phaseouts and complicated calculations but it did create new opportunities for wealth creation.

Your Annual Tax Return

The OBBBA directly reshapes the Form 1040 for high-income filers, creating a new and complex interplay between federal and state tax liabilities, the value of itemized deductions, and the ever-present Alternative Minimum Tax. The law offers a temporary and targeted reprieve on some of the TCJA's most discussed limitations (including the SALT limit) while simultaneously introducing new, permanent restrictions that claw back some of those benefits. Understanding these interrelated deductions and calculations is the first step in adapting your financial strategy.

The State and Local Tax (SALT) Deduction: A Temporary Reprieve with a Catch

You’ve likely encountered the headlines about the SALT deduction. For high-earners in states like California, New York, and our home state of New Jersey, the TCJA's $10,000 cap was a significant financial pain point. The OBBBA appears to offer major relief, but the details are critical.

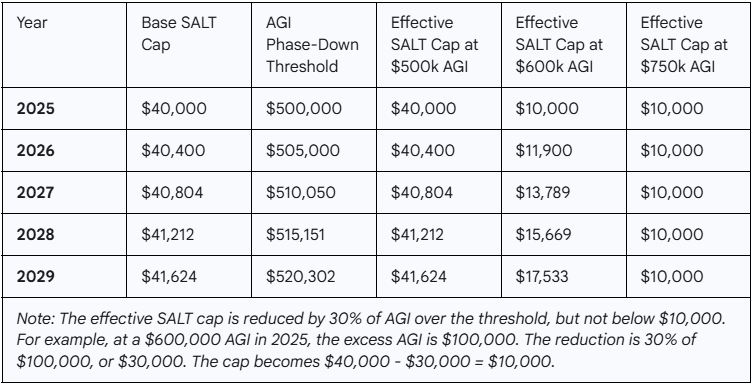

Section 70120 of the bill temporarily raises the SALT deduction cap to $40,000 for 2025, with a 1% annual inflation adjustment through 2029. It sounds like an undeniably attractive outcome for clients in high tax states.

But here’s where prudent investors need to pause. This relief is temporary as the cap reverts to a “permanent” $10,000 in 2030 (nothing in tax law is ever really permanent). More importantly, the higher cap comes with a new, aggressive income-based phase-down. For every dollar of modified AGI you earn above $500,000, your available SALT deduction is reduced by 30 cents, though it won't drop below the original $10,000 cap. As you can see in the table below, for someone with an AGI of $600,000 in 2025, the "new" $40,000 cap is functionally identical to the old $10,000 cap.

This structure creates a five-year window where strategic tax timing is important. Accelerating state tax payments into the 2025-2029 window could be beneficial, but only if it doesn't push your AGI over the phase-down threshold. For business owners, this makes Pass-Through Entity Tax (PTET) workarounds (if they are available for your entity type or state), which remain untouched by the bill, an even more essential tool for bypassing the individual SALT cap entirely.

The Return of Itemized Deduction Limitations (The "New Pease")

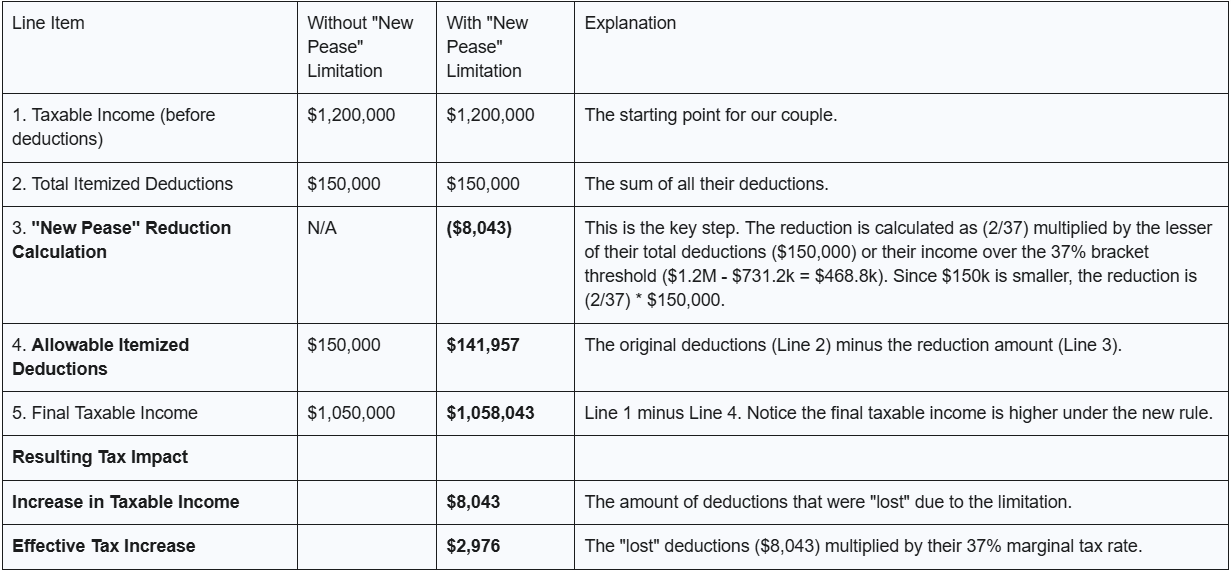

While the OBBBA gives a temporarily larger SALT deduction with one hand, it takes away some of its value with the other. Section 70111 revives a concept similar to the "Pease" limitation, which was suspended by the TCJA.

This new rule reduces your total allowable itemized deductions by a complex formula tied to your taxable income. In simple terms, it acts as a "stealth" tax increase. For a taxpayer in the 37% bracket, it means that each dollar of their itemized deductions, whether for mortgage interest, state taxes, or charitable gifts, no longer reduces their tax bill by the full 37 cents. Its value is diminished. This provision subtly increases the marginal tax rate for high-income households that itemize, demanding a more critical evaluation of the true value of each deduction when making financial decisions.

The Alternative Minimum Tax (AMT): A Narrower but Deeper Trap

OBBBA makes the higher Alternative Minimum Tax (AMT) exemption amounts from the TCJA permanent, which is good news that will keep millions of households out of the AMT's grasp. The AMT, a parallel tax system dating back to 1969, was designed to ensure the wealthiest households couldn't use loopholes to pay zero tax.9

However, there's a dangerous catch in Section 70107 of the new law: it doubles the phaseout rate for the AMT exemption from 25% to 50%. This means that while fewer people may fall into the AMT system, those who do will be hit much harder and faster.

The danger zone has shifted higher, now primarily targeting those with incomes over $1.25 million for joint filers. For these taxpayers, the new 50% phaseout rate is punitive. For every dollar of income earned above the phaseout threshold, 50 cents of their AMT exemption is clawed back, creating a cliff where the effective marginal tax rate can spike dramatically. This is especially hazardous for taxpayers with large AMT "preference items," like the bargain element on the exercise of incentive stock options (ISOs). The key takeaway is that high-income individuals, especially those with fluctuating income or significant equity compensation, must model for the AMT with renewed vigilance. The "safe" income level is higher, but the penalty for crossing the threshold is now far more severe.

New Constraints on Philanthropy: The Charitable Deduction Floor

The OBBBA introduces new friction to one of the most significant deductions for high-net-worth households. Section 70425 establishes a new floor for the charitable contribution deduction: individual contributions are now deductible only to the extent that their aggregate amount exceeds 0.5% of the taxpayer's adjusted gross income.

Think of this as a "deductible" on your philanthropy. A taxpayer with a $1 million AGI now faces a $5,000 floor. A gift of $5,000 results in a zero deduction; a gift of $6,000 results in a $1,000 deduction. This structure makes it inefficient to make moderate, consistent charitable gifts each year.

The clear strategic implication is a strong incentive to "bunch" charitable contributions. Instead of giving $10,000 annually for five years, a taxpayer is now far better off contributing $50,000 to a Donor-Advised Fund (DAF) in a single year. In that one year, they would secure a deduction for $45,000 ($50,000 gift minus the $5,000 floor) and could then recommend grants from the DAF to their chosen charities over the subsequent five years. This makes structured giving vehicles like DAFs and private foundations even more central to high-net-worth philanthropic planning.

A Shift in Wealth Transfer and Estate Planning

The OBBBA introduces two of the most significant changes to long-term, multi-generational wealth planning in decades. The first effectively eliminates the federal estate tax for all but the wealthiest families. The second creates a new tax-advantaged savings vehicle for minors that doubles as a powerful, yet complicated, wealth transfer tool. Together, these provisions demand a complete re-evaluation of traditional estate planning goals.

The $15 Million Estate & Gift Tax Exemption

Section 70106 of the OBBBA dramatically increases the basic exclusion amount for federal estate and gift taxes to a new, permanent $15 million base, effective for estates and gifts after December 31, 2025. This new, higher amount will continue to be indexed for inflation.

To appreciate the magnitude of this shift, consider that the exemption was just $2 million as recently as 2008. This increase solidifies a tax system where the federal estate tax is a concern for only a tiny fraction of the population (states can be completely different though). In 2021, only about 2,600 estates in the entire country paid any federal estate tax; this number will now fall even further.

For households with a net worth under $30 million (for a married couple), the federal estate tax has been effectively repealed. This fundamentally changes the primary objective of estate planning. For decades, the main goal was to use complex trusts to move assets out of the taxable estate. That concern is now gone. The new primary goal is income tax-basis planning. The focus shifts to maximizing the "step-up" in basis that heirs receive on inherited assets, which wipes out all embedded capital gains or converting pretax assets, like 401(k)s and Traditional IRAs, to post-tax assets, like Roths, while in retirement in a lower tax bracket than heirs. This creates a direct tension with lifetime gifting. With the exemption now so high, holding appreciated assets for the step-up is the optimal strategy for a much larger group of people. Financial advisors must pivot from a focus on estate tax minimization to a focus on strategically managing asset basis for the next generation.

"Trump Accounts": A Novel Vehicle for Intergenerational Wealth Transfer

Section 70204 of the OBBBA establishes new, tax-advantaged "Trump Accounts" for minors under 18. While presented as a savings vehicle, their structure makes them a uniquely powerful tool for intergenerational wealth transfer that can operate outside of traditional gift and estate tax limitations.

These accounts are treated like traditional IRAs, meaning investments grow tax-deferred. Contributions from individuals are limited to $5,000 per year (indexed for inflation). However, the crucial feature is the concept of "exempt contributions," which are not subject to this annual limit. These exempt contributions include "qualified general contributions" from nonprofit organizations or tribal governments, as well as contributions from a new government pilot program that provides a $1,000 contribution to an eligible child's account.

This structure provides a tax-advantaged "feeder" system for generational wealth. A high-net-worth family could, for instance, establish a family foundation and use it to make a "qualified general contribution" to fund Trump Accounts for their grandchildren. This mechanism could allow for the transfer of significant wealth outside the constraints of the annual gift tax exclusion. The funds are then locked in a highly protected, tax-advantaged environment, invested in low-fee index funds until the beneficiary turns 18, maximizing the potential for long-term compounding. Note, we are early in the application of these concepts and the IRS will likely issue further guidance on whether these constitute completed gifts and whether they fall under standard charitable giving or gifting limits.

Supercharging Private Investment: The QSBS Revolution

The OBBBA introduces transformative changes to tax incentives for private and venture investments. For high-net-worth individuals who are active accredited investors, these provisions create new opportunities to generate significant tax-free or tax-reduced returns.

The Qualified Small Business Stock (QSBS) Revolution

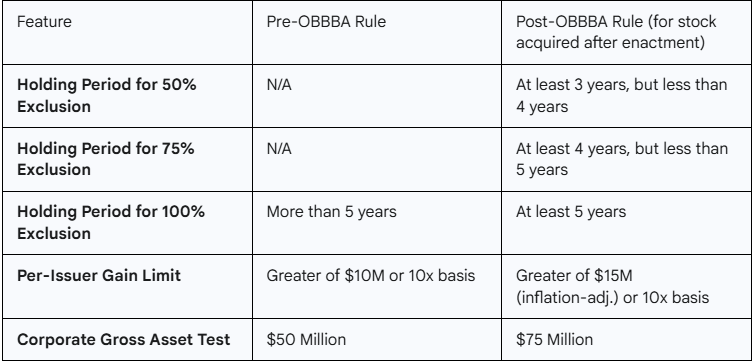

Section 70431 of the new law dramatically expands the gain exclusion for Qualified Small Business Stock (QSBS) under IRC Sec. 1202, a provision that was already one of the most powerful incentives in the tax code for early-stage investors.

The OBBBA makes three revolutionary changes:

- A New Tiered Exclusion: The previous all-or-nothing 5-year holding period for the 100% exclusion is replaced with a flexible, tiered structure. Investors can now exclude 50% of their gain if the stock is held for at least three years, 75% if held for at least four years, and 100% if held for five years or more.

- Increased Gain Limitation: The per-issuer cap on excludable gain is increased by 50%, from $10 million to $15 million (indexed for inflation).

- Expanded Company Eligibility: The gross asset test for a corporation to be considered a "qualified small business" is increased from $50 million to $75 million, expanding the universe of eligible companies.

These changes fundamentally reshape the risk/reward calculation for venture capital and angel investing. The new tiered structure de-risks these investments by providing a substantial tax break even if an exit occurs sooner than five years. Previously, an investor who sold after four years paid full capital gains tax; now, that same sale yields a 75% tax exclusion. For high-income investors, this makes direct angel investing and participation in venture funds significantly more attractive than investing in public markets.

The High-Earning Business Owner's Playbook

For individuals whose high income is derived from the ownership of pass-through businesses such as S corporations and partnerships, the OBBBA presents a complex duality. The law solidifies key deductions that benefit these entities but also makes permanent a significant limitation on their ability to use business losses.

The Qualified Business Income (QBI) Deduction: Enhanced and Solidified

The 20% Qualified Business Income (QBI) deduction under IRC Sec. 199A was a cornerstone of the TCJA for pass-through businesses. Its scheduled expiration was a major source of uncertainty. The OBBBA makes this crucial deduction “permanent,” providing long-term certainty for business planning.

In addition, Section 70105 provides a modest enhancement, increasing the taxable income limitation phase-in range for specified service trades or businesses (SSTBs), such as doctors, lawyers, and consultants, who were not allowed the deduction before from a threshold of $100,000 (for joint filers) to $150,000. This allows more professionals in this income range to claim a partial QBI deduction. While a significant victory, the core limitations remain for those at the highest income levels, meaning planning strategies to manage taxable income remain as relevant as ever.

Permanent Loss Limits vs. Aggressive Expensing for Business Owners

The OBBBA creates a permanent tension for business owners. On one hand, the law provides powerful incentives for investment. Sections 70301 and 70302 permanently restore 100% bonus depreciation and immediate expensing for domestic R&D, allowing businesses to immediately write off the full cost of major investments.

On the other hand, Section 70601 makes the limitation on excess business losses permanent. This rule limits the amount of net business losses a non-corporate taxpayer can deduct against their other, non-business income (like a spouse's salary) to an inflation-adjusted amount of approximately $500,000 for joint filers. I would have to agree with this one, $500,000 in losses in one year seems excessive.

This creates a direct conflict that must be carefully managed. A business owner could generate a large net operating loss through aggressive expensing, but the permanent loss limitation means they can only use a portion of that loss to offset other income. The rest is carried forward to offset future business income.

Re-evaluating Family Education Funding Strategies

The OBBBA introduces a sweeping overhaul of education-related tax benefits and financial aid rules. For high-income families, these changes require a complete re-evaluation of how to plan and pay for education.

The 529 Plan's Expanded Universe

Sections 70413 and 70414 transform the 529 savings plan from a "college savings" account into a comprehensive, "K-through-career" education funding vehicle.4 The definition of qualified expenses is massively expanded:

- K-12 Private Education: Qualified expenses now include curriculum, books, online tools, tutoring, test prep, and even educational therapies for students with disabilities. The annual limit on using 529 funds for these K-12 expenses is doubled from $10,000 to $20,000.

- Postsecondary Credentials: The law adds a comprehensive list of postsecondary credentialing expenses as a new category, covering tuition, fees, and equipment for programs that lead to professional licenses and certifications.

So the same account can now be used for private high school, a four-year degree, a coding bootcamp, or fees for a real estate license.

If you’re planning to use a 529 for K-12 expenses, it’s best to start as early as possible, perhaps as soon as you get married, setting up and funding your future child’s 529 to maximize its tax opportunities.

Overhaul of Graduate and Parent PLUS Loans

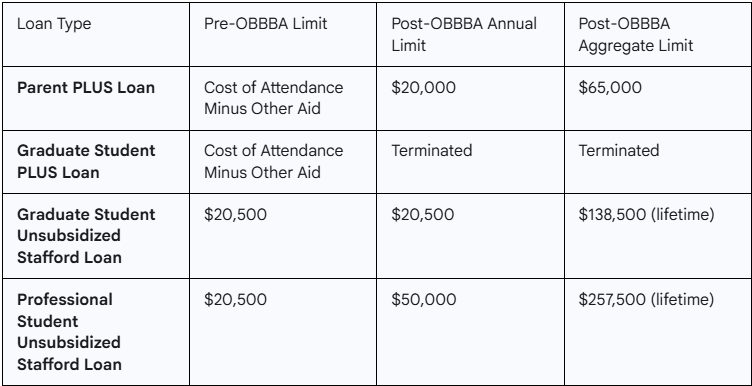

In a move that directly contrasts with the expansion of 529 plans, Section 81001 effectively dismantles the federal loan programs that have served as the primary financing mechanism for expensive degrees (including for most of my undergrad degree, Go Blue Hens!). The federal PLUS loan programs previously allowed parents and graduate students to borrow up to the full cost of attendance with no aggregate limit.

The new law terminates the Graduate PLUS loan program entirely for instruction periods starting on or after July 1, 2026. It also imposes new, highly restrictive lifetime borrowing limits. This will create a significant funding crisis for families planning to attend high-cost institutions. The era of relying on "easy" government financing for expensive degrees is over. Planning for these costs must now start earlier and involve a more deliberate mix of savings (in the newly supercharged 529 plans), private loans, and other family assets.

A Financial Aid Breakthrough for Business-Owning Families

In a targeted but profoundly impactful change, Section 80001 provides a major financial aid breakthrough for entrepreneurial families. The law excludes the net value of a family farm, a small business (with fewer than 100 employees), and a commercial fishing business from the asset calculation on the Free Application for Federal Student Aid (FAFSA).

This is a game-changer for families who may be "asset-rich but cash-flow poor." Previously, a family with a modest income but a valuable family business would be ineligible for need-based aid. Under the new law, the business asset is completely ignored. The family's aid eligibility will be based primarily on their income, potentially making their children eligible for thousands of dollars in institutional grants. This decouples the value of the family enterprise from the child's educational opportunities.

Conclusion: A Powerful Tool But Complex

So, is the One Big Beautiful Bill Act a guaranteed financial jackpot? Not universally. It is an incredibly powerful piece of legislation, yes, but like any tax bill, its benefits must be unlocked with skill, precision, and a clear, well-thought-out understanding of the long-term objective.

The OBBBA has rewritten the playbook for building and preserving wealth in America. It creates a distinct tension between long-term incentives for wealth creation, like the $15 million estate tax exemption and the expansion of the QSBS exclusion, and new, complex limitations on annual income tax planning, such as the SALT deduction phase-down and the new floor on charitable giving.

The bill is certainly better for high earners than the sunsetting of the TCJA’s tax brackets but don't get swept away by generalized hype or overly simplistic advice. A comprehensive review of your entire financial plan is non-negotiable. Success in this new environment will belong to those who recognize the scope of these changes and work with their advisors to adapt their strategies accordingly. Look beyond the immediate tax impact, considering your entire financial picture from today through your retirement years and even to your legacy planning, and making choices that aim for one primary outcome: paying less total income tax over your lifetime.

Purpose Built can provide the detailed tax forecasting and personalized financial planning needed to make informed decisions about the OBBBA, optimize your outcome, and move forward with confidence without missing any opportunities.

Contact Purpose Built today to see if we can help your family achieve financial independence.

Frequently Asked Questions (FAQ)

Q: Is the new $40,000 SALT deduction cap a sure thing for all high-earners?

A: No, it is not. While the cap is officially raised to $40,000 (with inflation adjustments) for 2025 through 2029, it comes with a new, aggressive phase-down. For every dollar of modified AGI you earn above $500,000, your available deduction is reduced by 30 cents. This means for a taxpayer with a $600,000 AGI in 2025, the effective cap is reduced back down to just $10,000. It's critical to calculate your specific situation to see if you benefit.

Q: With the $15 million estate tax exemption, do I still need an estate plan?

A: Absolutely. The focus of your estate plan simply changes. Instead of complex trusts designed to minimize federal estate taxes, the new primary goal is income tax planning for your heirs. The objective is to strategically manage assets to maximize the "step-up in basis," which eliminates capital gains tax on inherited property. Your plan should now focus on which assets to gift during your lifetime versus which to hold until death.

Q: How does the new QSBS rule change investment strategy?

A: It makes investing in qualified small businesses and venture capital funds significantly more attractive. The new tiered exclusion de-risks these investments by offering substantial tax breaks for holding periods as short as three years (50% exclusion). This provides more liquidity and a better tax outcome even if a company exits sooner than the traditional five-year mark, creating a powerful incentive to allocate capital to early-stage companies over public markets.

Q: What are "Trump Accounts" and how do they work?

A: "Trump Accounts" are a new tax-advantaged savings vehicle for minors established by the OBBBA. They grow tax-deferred like a traditional IRA and have a $5,000 annual contribution limit from individuals. However, their unique feature allows for potentially unlimited "qualified general contributions" from nonprofits, which could include a family foundation. This creates a powerful, albeit complex and not-yet-fully-defined, tool for intergenerational wealth transfer that may operate outside of normal gift tax limits.

Q: What is the single most important action I should take in response to the OBBBA?

A: The single most important action is to schedule a comprehensive review of your entire financial plan with a qualified advisor. The OBBBA's provisions are deeply interconnected, changes to SALT deductions affect itemized deductions, which in turn impact your overall tax liability. A holistic analysis is required to understand how these new rules interact and to build a new strategy that optimizes your taxes, investments, estate plan, and philanthropic goals for this new landscape.

Final Thoughts: Seizing the Moment in a New Tax World

The One Big Beautiful Bill Act isn't just another tax law, it's a shift in the rules of wealth creation, offering immense opportunity for those who act decisively. But these powerful incentives, from the $15 million estate exemption to the revamped QSBS rules, are not automatic; they must be actively seized.

With complex new phase-outs and limitations, waiting or making unguided decisions could mean leaving significant money on the table. It is critical to look beyond any single provision and understand how the entire bill impacts your unique financial picture—from your annual income to your generational wealth transfer goals. Tax strategies are only valuable when they align with your investments, business structure, and legacy.

Purpose Built can help you run the numbers, model the intricate effects of the OBBBA, and design a cohesive strategy to capture the opportunities available before they evolve. Let’s make the most of this new landscape, before the biggest windows of opportunity close. Contact us today.

About the Author

Sean Lovison, CPA, CFP®, is a fee-only financial planner based in Moorestown, New Jersey, serving clients virtually nationwide. After spending 14 years as a corporate chief financial officer (CFO), receiving and designing compensation plans, he decided to help others navigate their plans.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Sean Lovison and Purpose Built Financial Services (PBFS), unless otherwise specifically cited. The material presented is believed to be from reliable sources, and no representations are made by our firm regarding other parties' informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant, or legal counsel prior to implementation.

The information on this site is provided "AS IS" and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, PBFS disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. PBFS does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall PB be liable for any direct, indirect, special, or consequential damages that result from the use of, or the inability to use, the materials on this site, even if PB or a PB-authorized representative has been advised of the possibility of such damages. In no event shall Purpose Built have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

.jpg)