5 Key Points from the Article

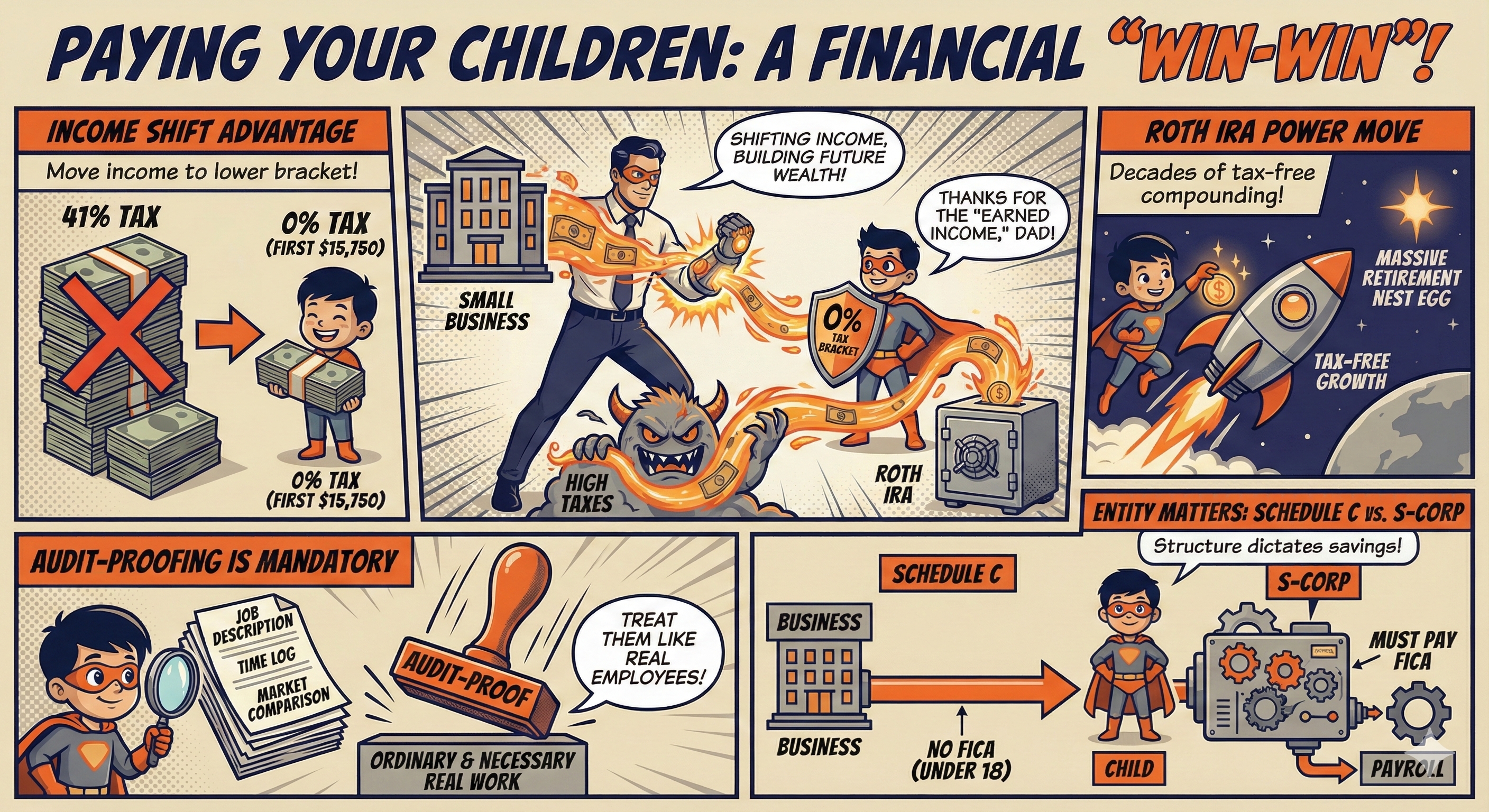

- The "Income Shift" Advantage: Moving business income to your children can shift tax liability from your high marginal bracket (potentially 41% or more) to your child’s 0% bracket, thanks to the standard deduction ($15,750 in 2025).

- Entity Structure Matters: Schedule C (Sole Proprietorships/LLCs) offers the greatest savings because wages paid to children under 18 are exempt from FICA (Social Security and Medicare). S-Corps do not naturally have this exemption although there is a way around it.

- The Roth IRA Power Move: By paying your children "earned income," they become eligible to contribute up to $7,000 (2025) or $7,500 (2026) into a Roth IRA, where decades of tax-free growth can build a massive retirement nest egg.

- Audit-Proofing is Mandatory: The IRS requires that work be "ordinary and necessary" and pay be "reasonable" for the market. You must keep a job description, time log, and Market Comparison on file.

- The Documentation Trail: You must treat your children like real employees. This includes issuing a W-2, filing an I-9 to verify employment eligibility, and actually transferring the funds to a bank account in their name.

Employing your children is one of the most sophisticated "win-win" tax strategies available to small business owners. It allows you to move money from your high tax bracket into your children’s zero-tax bracket, effectively funding their future, ideally with a Roth IRA, using tax-deductible business dollars.

For households with income in the $500K to $600K range, where the SALT deduction is phased out, this strategy offers exceptional power in 2025 and 2026. If you find yourself in the phaseout range and equate to an effective tax rate of 41%, better to give that to your child instead of the IRS.

Here is your guide to the logistics, rules, and specific examples for your family.

Why Pay Your Kids? (The "Tax Bracket Shift")

The primary driver here is income shifting. When you keep $15,000 in business profit, you might pay 24%–37% in federal income tax, plus self-employment and state taxes.

However, by paying that $15,000 to your child as a legitimate business expense (more on what is legitimate later):

- The Business Deduction: Your business deducts the $15,000, lowering your own taxable income.

- The Standard Deduction: In 2025, the standard deduction for a single filer is $15,750 ($16,100 in 2026). If your child has no other income, they pay $0 in federal income tax on that first $15,750.

- Family Wealth: The money stays in the family but is now in your child’s name, ready to be used for college savings or a Roth IRA.

What is Legitimate?

The IRS is particularly skeptical of payments made to family members. To qualify as a deductible business expense, the wages paid to your children must meet two specific criteria: they must be ordinary and necessary for the business, and the amount must be reasonable.

Necessary Work: This means the work performed must actually benefit your business. If you weren't hiring your child to do these tasks, would you eventually have to hire a third party or do them yourself? Playing video games in the office or "modeling" for a single Instagram post generally won't pass the "necessary" test (no matter how cute your child is).

Reasonable Pay: The IRS defines "reasonable" as the amount that would ordinarily be paid for like services by like enterprises under like circumstances. In plain English: You must pay your child what you would pay a stranger for the same job. Paying a 13-year-old $100/hour to shred paper is an "unreasonable" wage and will likely be reclassified as a gift (which is not tax-deductible). However, paying them $15–$20/hour, the market rate for office support, is perfectly defensible.

The job and tasks that you hire your children to do must also be age appropriate. There is limited guidance on this but much like the over payment examples above, it would be pretty unlikely to hire your 13 year old to write complex articles or trust them to draft client documents. Some age appropriate examples of tasks I have for my daughters include:

Age 13: Cleaning the office, shredding non-confidential drafts, organizing supplies, restocking the coffee station, running errands such as picking up bagels/lunch (our office right off our town’s Main St so this can be done by walking or bike), and assembling marketing folders.

Age 16: Managing CRM data entry (checking no data is missing), proofreading client newsletters, updating website links, ensuring compliance documents are in their proper folders, running errands such as going to the post office, and drafting social media captions.

Potential taxes can vary widely depending on the age of your children and the industry you’re in.

How to Prove It

Even if you follow the guidance above, you will still need to document your adherence. Here are some documents you should prepare and have on file to help you create an "Audit-Trail" in case of an audit:

Job Description: Write a simple one-page document outlining the child's title, responsibilities, and hourly rate. Here in NJ, the minimum wage is $15 which creates a pretty justifiable wage floor and pretty good for a minor. However, I may still be stuck on making $5.15 at Dairy Queen for my first job.

The Time Log: A log with dates, start/end times, and specific descriptions (e.g., "Scanning 50 insurance contracts" vs. "Helping") is your best defense.

Market Comparison: Keep a screenshot of a job posting on a site like Indeed or LinkedIn showing the local market rate for an "Administrative Assistant" or "Office Clerk" to justify the hourly rate you chose.

Examples of Savings Impact

Using fictional numbers, neither of my children were interested in working this much for their father this year, for a Schedule C business. We’ll see if they decide to want to work more with me later…

Daughter Age 16: The Admin & Marketing Assistant

- The Tasks: Managing CRM data entry, proofreading client newsletters, updating website links, and drafting social media captions.

- The Strategy: By paying your child $5,000 annually for services performed for your business (reported on Schedule C), you can achieve significant tax savings.

- Federal Income Tax Savings: If you are in the 24% tax bracket, you save approximately $1,200 or more in income taxes. This saving could increase to $2,080 if you are affected by the SALT deduction phase-out.

- Payroll Tax Savings: You save an additional $765 in FICA (payroll) taxes.

- State Tax Savings: Depending on your state, you may realize further savings on state income taxes.

Daughter Age 13: The Office Support Specialist

- The Tasks: Dusting and cleaning office, shredding non-confidential drafts, organizing supply closets, restocking the coffee station, and assembling marketing folders.

- The Strategy: Pay her $2,500/year. This is a great "starter" wage that teaches work ethic while shifting $2,500 of your highest-taxed income into her 0% bracket.

- Federal Income Tax Savings: At the 24% tax bracket used earlier, your savings will be approximately $600 or more in income taxes. This saving could increase to $1,040 if you are affected by the SALT deduction phase-out.

- Payroll Tax Savings: You save an additional $382 in FICA (payroll) taxes.

- State Tax Savings: Depending on your state, you may realize further savings on state income taxes.

Combining the two and both forms of taxes, the total savings would be more than $2,947 if you’re a Schedule C filer!

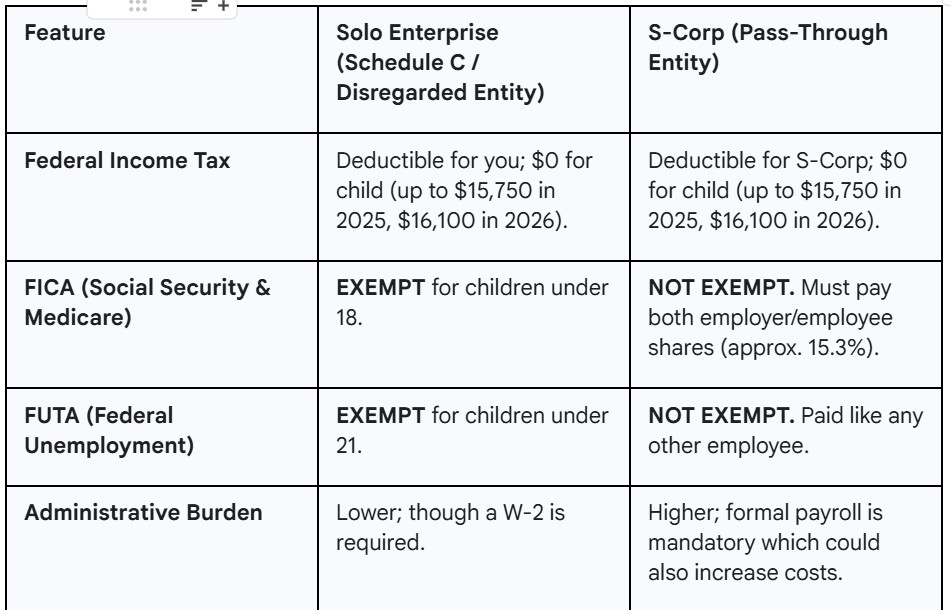

Schedule C vs. S-Corp: The "Payroll Tax" Difference

Sadly, nothing with the IRS is simple nor the same for everyone. Your business structure dictates exactly how much you save. This is a critical sticking point: the IRS treats "parents" and "corporations" differently.

Pro-Tip for S-Corps: Because an S-Corp is a separate legal "person," the IRS doesn't see the child working for a parent; they see them working for a corporation. To regain the FICA exemption, some owners use a Family Management Company (a separate Schedule C entity) to hire the kids and bill the S-Corp for those services. This gains the deduction back but creates an extra layer of complexity.

The Mechanics: How to Actually Execute This

Regardless of your structure, the first step is the same: Open a dedicated bank account for your child. Do not just keep the money in your own account. To prove the expense is "ordinary and necessary," the money must actually change hands.

Part A: The Simplified LLC Approach (Schedule C / Disregarded Entity)

If you are a solo practitioner or a simple LLC, you have the "Express Lane." Because children under 18 working for their parents in an unincorporated business are exempt from FICA (Social Security/Medicare) and FUTA (Federal Unemployment), the process is remarkably simple.

- The Payment: Simply transfer the funds from your business checking to their personal checking account (ACH, Venmo, or Check). You can do this monthly or as a lump sum after projects are completed.

- The Payroll Filing: You do not need to hire a payroll company. Since no taxes are being withheld (Federal, Social Security, or NJ State), there is no quarterly reporting required.

- The Year-End W-2: You are still required to issue a W-2 to the child so they have a record of "Earned Income" (crucial for the Roth IRA). You can do this for free directly through the Social Security Administration’s Business Services Online (BSO) portal.

- State Requirements: Each state is different so you will need to verify the rules in your state. In New Jersey, you generally do not need to file NJ state payroll reports if the child’s income is below the $10,000 threshold and no tax is withheld.

Part B: The Formal S-Corp Approach

If your business is an S-Corp, the IRS views the corporation as a separate entity and that means you must run formal payroll, and you must pay payroll taxes (FICA/FUTA). You have three main ways to handle this:

1. Full-Service Payroll (Recommended)

Providers like Gusto, QuickBooks Payroll, or ADP Small Business handle everything. You enter the hours, and they calculate the taxes, file the quarterly forms (941s), and issue the W-2 at year-end.

- Pros: "Set it and forget it"; total compliance.

- Cons: Monthly service fees (usually $40–$80/month).

2. Self-Filing with Software

You can use a basic software like Tax1099 or eFileMyForms to handle the filings manually at a lower cost. You would still be responsible for calculating the withholdings yourself.

3. The "DIY" Manual Method (The Hard Way)

If you choose to do this yourself, you must manually calculate and pay the following for every paycheck:

- Employee Share: Deduct 7.65% for Social Security and Medicare from their gross pay.

- Employer Share: Your business pays an additional 7.65% on top of their gross pay.

- The Math: If you pay Zoe $5,000, your business actually pays $5,382.50, and Zoe receives $4,464.68.

- Reporting: You must file Form 941 quarterly and Form 940 annually with the IRS, plus make timely tax deposits through the EFTPS system.

The Purpose Built Strategy: If the S-Corp administrative burden and the 15.3% payroll tax cost seem too high, we can discuss setting up a Family Management Company (a Schedule C entity) that hires the kids and bills the S-Corp, effectively moving you back into the "Simplified LLC" lane.

BOTH: A Compliance Issue, The I-9 Form

Even though you know your kids are your kids, the Department of Homeland Security requires every employer to maintain a Form I-9 for every employee. This form must be completed within three days of their first day of work.

The requirement is that you need to examine their Birth Certificate and Social Security card (or Passport) and then sign the form. I’m sure you won't need to actually look at the documents to complete these for your child, but you should ensure you have the actual documents you say you looked at in case of an audit. It would be rather embarrassing to learn during an audit that you lost their birth certificate when you claimed you looked at it and now don't have it.

You don't file the I-9 with the government, but you must keep it in your files for three years after they are hired or one year after they leave.

The Ultimate Power Move: The Roth IRA

Now that you have sorted out all the blocking and tackling of how to actually pay your children and record the income, what should your children do with the money? You know the kids' vote: Starbucks, Chipotle, and skin care products they learned about on TikTok! Those items may be specific to my girls, but I am sure yours will want to spend it as well.

There is, of course, a better option: once your children have that W-2 "earned income," they are eligible to open a Roth IRA:

- 2025 Contribution Limit: Up to $7,000 (or 100% of their earnings, whichever is less). The limit is $7,500 in 2026.

- The Magic of Compounding: If a 13-year-old invests $7,000 today at a 7% return, that single contribution could grow to over $230,000 by age 65, all entirely tax-free!

The tricky part is convincing a 13-year-old to invest all their earnings now for a possible payoff in 32 years. If you have successfully accomplished this feat, congratulations; you are possibly the world’s greatest salesman and parent. I salute you and please reach out to me and provide the deets on how you did it.

Most parents do a little mathematical gymnastics where they will “gift” any amount of money earned to the child so they can reap the benefits of the work they put in, hopefully reinforcing the value of hard work, while at the same time using the funds the child earned to contribute to a custodial Roth IRA in their name.

Now, a Roth IRA is not without some risks. Once the child reaches the age of majority, which varies by state but is usually between 18 and 24, the child has full access to the funds. This means if your child ends up being a spendthrift, they could withdraw the funds, incurring the tax penalties on the growth, and use the funds to purchase whatever they want. The way this risk is often mitigated is by keeping the account a secret from the child.

Ready to Build Your Family's Financial Legacy?

Tax strategies like these are exactly why we started Purpose Built. We don't just look at your business or taxes in a vacuum; we look at your entire family's financial picture to ensure you aren't leaving money on the table. We believe that good tax planning is the key to increasing investment returns, not high cost overly complicated investments.

Strategies like paying your child require precision and proper documentation to be effective. Don't leave your tax savings and wealth building to chance.

Contact Purpose Built Today to schedule a strategy session. Let’s make sure your 2026 tax plan is working as hard as you are.

Frequently Asked Questions (FAQ)

Q: Do I really have to issue a W-2 to my kids?

A: Yes. While it adds a small administrative step, the W-2 is the "gold standard" of proof for the IRS. It is also required to justify the contribution to a Roth IRA, as the IRS looks for reported earned income to support those accounts.

Q: Can I pay my child for "modeling" or chores at home?

A: No. Chores (like cleaning their own room) are not business expenses. Modeling can be legitimate, but it is highly scrutinized by the IRS; the work must actually benefit your business operations or marketing efforts.

Q: At what age can I start paying my children?

A: While there is no hard "minimum age" in the tax code, the work must be age-appropriate. Most professionals recommend starting when the child is old enough to realistically perform a task, usually around age 7 or 8.

Q: Can my child spend the money, or does it have to go to the Roth IRA?

A: It is their money. They can spend it on Starbucks or video games. However, many parents use a "matching" strategy: they give an equivalent amount to the child they are allowed to spend while using the child’s funds to contribute to their Roth IRA.

Q: What happens when they turn 18?

A: Once they turn 18, you lose the FICA (Social Security/Medicare) tax exemption in a Schedule C business. You can still pay them and deduct the wages, but both you and the child will have to pay the standard 15.3% payroll taxes.

Final Thoughts

Employing your children is more than just a tax loophole; it’s a lesson in financial literacy. By the time your daughters reach adulthood, you don’t just want them to have a savings account, you want them to understand the importance of work ethic, a tax-free retirement foundation, and a firsthand look at how entrepreneurship creates family wealth. In a landscape of rising tax rates and phased-out deductions, it is perhaps the most efficient way to keep more of what you earn within your own family circle.

We can help you build the environment for your children to be financially fluent while saving you taxes and building your wealth in the fastest way possible. Reaching financial independence as soon as possible is the best way to have even more time to pass along your family wisdom and heritage.

About the Author

Sean Lovison, CPA, CFP®, is a fee-only financial planner and founder of Purpose Built Financial Services. After spending 14 years as a corporate chief financial officer (CFO), receiving and designing compensation plans, he decided to help others navigate their plans.

Purpose Built Financial Services is a state registered (PA and NJ) advisor but legally able to virtually serve high-earning households in all 50 states. While we specialize in the unique tax complexities of the NJ/NY/PA tri-state corridor, our 'Personal CFO' model is designed for tech leaders nationwide who require sophisticated equity and tax coordination.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Sean Lovison and Purpose Built Financial Services (PBFS), unless otherwise specifically cited. The material presented is believed to be from reliable sources, and no representations are made by our firm regarding other parties' informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant, or legal counsel prior to implementation.

The information on this site is provided "AS IS" and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, PBFS disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. PBFS does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall PB be liable for any direct, indirect, special, or consequential damages that result from the use of, or the inability to use, the materials on this site, even if PB or a PB-authorized representative has been advised of the possibility of such damages. In no event shall Purpose Built have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

.jpg)