5 Key Points

- Prioritize Your Own Financial Foundation: The "oxygen mask" principle is paramount. Secure your own retirement savings, emergency fund, and tax-advantaged accounts (like a 401(k) and HSA) before taking on the financial burdens of others.

- Strategic Education Planning: For high-earning households, 529 plans are often the superior choice for education savings due to their tax advantages and minimal impact on financial aid eligibility compared to custodial accounts.

- Proactive Parental Planning: Initiate empathetic conversations with your parents about their finances and long-term care wishes before a crisis occurs. Consider hiring a professional financial planner for a one-time engagement to help with this sensitive topic.

- Long-Term Care Considerations: While long-term care insurance can be a solution, high-earning families may find that self-insuring is a more practical option. Understanding the pros and cons of both is crucial for financial peace of mind.

- Professional Guidance for a Multigenerational Plan: The article highlights the importance of a comprehensive financial plan that addresses all three generations. A professional can help you create a strategic blueprint that coordinates goals and ensures your own financial security is not sacrificed.

Intro

The demands of modern life can be overwhelming, but few challenges are as complex and emotionally charged as supporting multiple generations at once. This unique position, often referred to as being part of the "Sandwich Generation," places middle-aged adults in the middle of a dual caregiving role, responsible for providing both financial and emotional support for their aging parents and their own children.

This situation is far from rare. According to a 2021 Pew Research Center survey, nearly a quarter of U.S. adults (23%) are part of this group. The demographic most likely to find themselves in this role are those in their 40s, with over half (54%) of this age group having a living parent age 65 or older and also either raising a child under 18 or financially supporting an adult child. However, the experience is not confined to one age group, with a growing number of adults in their 50s and 60s also feeling the effects. This article is a guide for navigating this multi-layered challenge, providing a clear and compassionate roadmap to help individuals balance their parents' needs, their children's future, and their own financial security.

Part I: The Shifting Landscape of Family Finances

The challenge of being in the sandwich generation is rooted in both economic (negative) and demographic (positive) shifts. The demographic shift is a good one, Americans are living longer, but economically young adults are struggling to achieve financial independence.

The Unavoidable Costs of Caregiving

The financial strain of dual caregiving is not abstract; it can be quantified through the staggering costs associated with supporting each generation.

The Price of Raising a Child

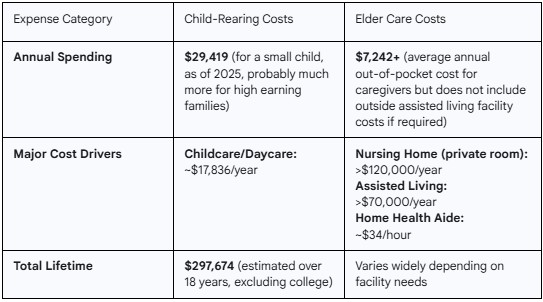

Raising a child is one of the most significant financial undertakings a family can face. A recent LendingTree study, conducted in 2025, found that the annual cost to raise a small child had jumped to $29,419, representing a 35.7% increase since a similar study in 2023. Over 18 years, costs add to $297,674, up 25.3% from the previous report. Higher earning families might find these numbers low as you may also send your children to additional programs and enrichment activities, such as club sports and robotics teams, that may be close to double those numbers.

And not to pile on but these figures don't even include the cost of a college education!

The Soaring Cost of Elder Care

On the other side of the equation are the often-staggering and unpredictable costs of elder care. For many families, this is a sudden expense that can quickly deplete a lifetime of savings. The median national cost for a private room in a nursing home is over $120,000 per year, while an assisted living community can cost more than $70,000 annually. For those who wish to keep their parents at home, the cost of a home health aide is still substantial, at around $34 per hour. These expenses can be a major challenge for families, especially given that Medicare only covers a limited portion of these services under specific circumstances. Many states have a Medicaid program that may cover long-term care, but it often comes with strict income and asset requirements, requiring individuals to "spend down" their assets to remain eligible. But even if eligible, many high earning families are reluctant to send their parents to Medicaid covered facilities unless they first “buy in” to better ones first.

The Compounded Impact on You

The pressure of these dual financial responsibilities doesn't just empty bank accounts; it compromises the middle generation's ability to earn and save for their own future. Most high earning households tackle caregiving via outsourcing but if one spouse decides to provide caregiving, it often requires a significant time commitment, with one in four family caregivers spending 41 hours or more per week on these duties. This time commitment can lead to substantial professional sacrifices. A 2023 study found that 27% of working caregivers shifted from full-time to part-time work, 16% turned down a promotion, and 16% left their jobs entirely for a period of time. For women, who make up the majority of caregivers, this can have a devastating long-term impact, with the total lifetime cost of caregiving in lost wages and benefits estimated to be as high as $324,044.

The financial pressure is compounded by the emotional toll. According to a University of Michigan study, people in the sandwich generation are twice as likely to report financial difficulty and more likely to report substantial emotional difficulty than their non-sandwiched peers. Unsurprisingly, nearly half of all caregivers report facing major financial consequences as well, such as draining savings or falling into debt, as a direct result of their responsibilities.

The following table visually represents this dual financial pressure, providing a clear overview of the costs that create the squeeze on the sandwich generation.

The sandwich generation faces a self-perpetuating cycle of financial instability. Young adults burdened by debt are returning home, often referred to as the "boomerang generation," while aging parents are living longer and requiring expensive long-term care. This dual pressure drains the middle generation’s savings, making it difficult to save for their own retirement and increasing the risk they will become a burden on their children.

This situation is worsened by rising expenses and reduced income. Inflation drives up costs for childcare and long-term care, while caregivers often cut back on work hours or leave their jobs to meet caregiving demands. This combination of higher costs and lower earning potential creates severe financial instability.

Furthermore, the emotional toll of caregiving is intense. The stress and burnout can impair a person's ability to make sound financial decisions, preventing them from creating the proactive plans necessary to manage their complex finances. This psychological burden is a direct obstacle to effective financial planning.

Part II: The Strategic Blueprint for Financial Stability

Effective financial planning for the sandwich generation requires a strategic, multi-layered approach that addresses the needs of each generation while safeguarding the financial future of the caregiver.

Your Foundation First: Prioritizing Your Own Financial Health

Before attempting to solve the financial problems of others, it is imperative to secure your own financial foundation. The metaphor of putting on your own oxygen mask before helping others is a powerful principle here. To be a reliable source of support for your family, you must first ensure you won’t become a financial burden on them later.

Maximizing Retirement Savings. The first priority should be your retirement savings. At a minimum you need to contribute at least enough to your workplace retirement plan to get the full employer match, which is essentially "free money." For high earning households this amount may be significantly more to maintain your style of living in retirement. Understanding and saving that amount and saving it, will ensure you reach your financial goals as well as drastically reduce stress.

The Power of Catch-Up Contributions. For people who will be 50 or older by the end of the calendar year, it is possible to contribute pre-tax an extra $1,000 to an IRA and $7,500 to workplace plans like a 401(k) in 2025. For those aged 60-63, this limit increases to $11,500 for 401(k) plans in 2025. Taking advantage of these higher contribution limits can make a major difference in a short period of time and provide valuable tax savings to households in higher tax brackets.

Using Tax-Advantaged Accounts. The accounts used for savings are as important as the amount saved. Tax-advantaged accounts like a 401(k) or IRA allow your investments to grow with tax benefits, this is especially valuable for high income households. Another powerful pre-tax account, often overlooked or used incorrectly, is a Health Savings Account (HSA). An HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified health expenses. This makes it an excellent vehicle for saving for future medical costs, both for yourself and your parents (if they become a qualifying dependent), and can serve as an additional source of income in retirement.

Building an Emergency Fund. A robust emergency fund is a non-negotiable safety net. For members of the sandwich generation, who face unexpected medical bills or caregiving needs, a cash reserve of at least six to twelve months of living expenses is recommended, although this may be more if someone in your household works in a volatile field or has a veritable income. This fund protects long-term savings from being tapped for a short-term crisis and provides a crucial sense of security.

Securing Your Children’s Future

Planning for a child's education is a core component of my high income household clients. A dual approach is often most effective: using the right financial tools while also instilling sound financial values.

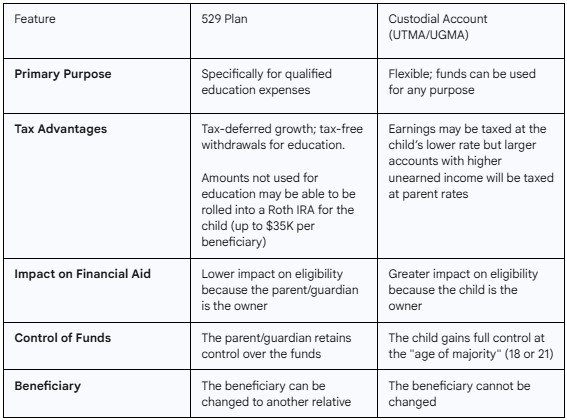

Education Savings Strategies. The most common education savings tool for high earners are 529 plans. Custodial accounts (UTMA/UGMA) are sometimes used but they have some negatives when the balances become material and they produce unearned income which then becomes subject to the kiddie tax. A 529 plan is a tax-advantaged account designed specifically for education savings. Contributions grow tax-deferred, and withdrawals are tax-free if used for qualified education expenses (and may provide state level tax deductions). Because a parent, grandparent, or guardian owns the account, it has a lower impact on financial aid eligibility as measured by the FAFSA.

In contrast, a custodial account, such as a UGMA or UTMA, is a financial account set up by an adult to hold assets on behalf of a minor. The funds in these accounts are not restricted to education and can be used for any purpose once the child reaches the "age of majority" (typically 18 or 21). However, this flexibility comes with a trade-off. The minor is the legal owner of the account, which can significantly hurt their eligibility for financial aid. As mentioned in the opening paragraph, the earnings in the account may also be subject to the parents tax rate due to the “kiddie tax.”

The decision between these two options depends on a family’s specific goals and the income of the family. The following table provides a clear comparison of the key features of each account.

Cultivating Financial Literacy. You don’t often see this discussed in planning circles but just as important as saving is teaching. A key part of the financial plan is to empower your children to become financially independent adults, reducing the likelihood that they will need to rely on you in the future. This involves open and honest conversations about the family budget, teaching them the difference between needs and wants, and involving them in discussions about saving for long-term goals like a car or college. Outside help may even be needed in this area as children often are resistant to advice their parents offer no matter how valuable. I myself decided to hire a college counselor to not just help with the college selection process but educate my daughter (15) on the cost of college along with the financial return associated with majors.

Allowing your child to graduate with a degree from a low paying field may be okay, but you can’t allow them to go into hundreds of thousands of dollars of debt to do it. Even if you have the funds available, those resources may be better spent helping them get set up as a young adult than spent on an overly prestigious degree.

Navigating Your Parents’ Finances

The final piece of the financial blueprint involves navigating the complex and sensitive area of your parents’ finances. This requires empathy, careful planning, and an understanding of the resources available to them.

Understanding Their Financial Picture. The first, and often most challenging, step is to initiate a conversation with your parents about their financial situation, long-term care preferences, and legal documents. This should be approached with empathy and respect, framing the discussion around ensuring their wishes are honored and their security and well-being are protected. One valuable technique is to ask about their goals, hopes, and desires for the future, with the financial discussion serving as a way to determine how to achieve them. Once the lines of communication are open, a caregiver can help organize their parents’ financial and legal documents, including bank accounts, real estate holdings, wills, trusts, and healthcare directives. If getting into that level of detail is difficult for you, consider offering to hire a financial planner to do a one-time financial plan for your parents. I have personally done engagements like this for clients' parents, it can be very valuable to learn all the details about your parents financial situation without you having to be the one to appear prying.

Long-Term Care Insurance. Long-term care insurance (LTCI) can help cover the significant costs of elder care, including assisted living, home health, and respite care, which standard health insurance or Medicare typically don't. The ideal time to buy a policy is usually between ages 50 and 65, when premiums are more favorable due to better health. However, these policies aren't a “silver bullet” or a complete solution; they can be costly with increasing premiums. For high earners, self-insuring might be more practical, but LTCI can reduce anxiety about potential future care expenses.

Government and Community Support. Caregivers are not expected to manage this burden alone. There are a number of government and community resources available to provide financial, physical, and emotional support.

- Medicaid: While often a last resort, the state-run Medicaid program can be a lifeline for individuals who need long-term care but have limited income and resources. A person may be eligible if they require long-term care and meet specific financial criteria, including income and resource limits. It is important to contact the state’s Medicaid agency directly to determine eligibility and apply. There are Medicaid consultants that can specifically help you with the process if you are looking for professional help but they vary by state and need to be properly vetted before deciding to use them.

- National Family Caregiver Support Program: Established in 2000, this program provides grants to states and territories to fund a range of support services for family caregivers, including information, counseling, support groups, and respite care. Respite care, in particular, offers temporary relief from caregiving responsibilities, which is crucial for preventing burnout.

- Find Local Resources: Eldercare Locator, a public service of the Administration for Community Living, was set up as a governmental service to help connecting you to services for older adults and their families.

Tax Benefits. The federal tax code offers some relief for those supporting an aging parent or other relative. Caregivers may be eligible for three key tax credits:

- The Credit for Other Dependents: This credit offers a maximum of $500 per dependent. A caregiver may qualify if they can claim their parent or elderly relative as a dependent, and the loved one does not need to live with them to qualify.

- The Child and Dependent Care Credit: This credit can be claimed for a qualifying individual, including an elderly parent who is physically or mentally incapable of self-care, for whom care was paid so the taxpayer could work or look for work. The maximum credit is $3,000 for one qualifying individual or $6,000 for two or more.

- Health Savings Accounts: Funds saved pre-tax can be used for parental care if they are a qualified dependent as defined by the IRS, which they might be if you are providing most of their financial support.

The resurgence of multigenerational households in the U.S. is not a fleeting trend. It will continue to become more common due to the economic pressures and demographic changes we discussed earlier. This changing structure requires a multi-generational financial plan that coordinates goals across all three generations, rather than treating them as separate financial silos. The most effective financial strategies are those that acknowledge this interconnectedness, ensuring that resources and responsibilities are fulfilled while making sure you reach your own financial goals!

Beyond financial solutions, non-financial support like emotional aid, logistical help, and community resources are crucial for caregivers' well-being and maintaining their earning potential without intense emotional fatigue.

Part III: Beyond the Numbers: The Emotional & Practical Guide

While financial planning is essential, it is only one part of the solution. The emotional and logistical aspects of caregiving are equally important to manage for the long-term well-being of everyone involved.

The Importance of Open Communication

Financial discussions are rarely just about the numbers; they are about deeply held values, control, and independence. A purely logical, financial approach will fail if it doesn’t first address the emotional difficulties and concerns.

Talking to Your Parents. It's crucial to approach these conversations with empathy and respect. Aging parents may be hesitant to discuss their finances because they are grappling with a loss of independence. Reminding them that they are still in control and that the goal is to help them continue living their lives on their terms can help build trust and open a productive dialogue. Experts recommend starting the conversation early, before a crisis occurs, and in a calm, stress-free environment. It could help to bring in a professional advisor, preferably yours who knows your background, so that the conversations between you and your parents can focus on the emotional aspects of this life change.

Talking to Your Children. With younger children, your focus should be on education. Educate them on making income, budgeting, and being able to save to reach their goals. With adult children, open communication is also key. It is important to be honest with them about your financial situation, set clear expectations, and define boundaries. This approach is not about guilt or blame; it is about promoting their financial literacy and independence, which is a vital part of helping them achieve long-term success.

Engaging with Siblings and Spouses. Caregiving should not be a one-person job. It is essential to communicate with siblings and spouses to share both the responsibilities and the costs. This may require difficult conversations, but finding a way for others to help by providing financial assistance, taking on logistical tasks, or offering respite care is critical for alleviating the strain on the primary caregiver. Understanding the burden on the primary caregiver, often the sibling who lives closest to the parent, goes a long way.

The Legal & Logistical Essentials

A proactive approach to legal and logistical planning can save a family immense stress, time, and money down the road.

Essential Legal Documents. Preparing the right documents for yourself and your parents is a major component of any multi-generational plan and if it has not been done yet, needs to be started immediately. This includes:

- Durable Power of Attorney (DPOA): This document authorizes another person to act on your behalf in financial and legal matters if you become unable to do so yourself. There are two types: an immediate DPOA, which is effective right away, and a springing DPOA, which only becomes effective upon incapacitation.

- Will: A will is the cornerstone of any estate plan, outlining how property will be disbursed after death and naming an executor to manage the estate. Without a will, a court will decide how assets are distributed through a process called probate which can be slow and expensive depending on the state.

- Advance Medical Directives: These documents communicate your wishes regarding medical treatment in the event you cannot express them yourself. This can include a living will, which allows you to approve or decline certain types of medical care, and a durable power of attorney for health care, which appoints a representative to make medical decisions for you.

There are additional documents some experts recommend including a POLST (Physician Orders for Life-Sustaining Treatment) or MOLST (Medical Orders for Life-Sustaining Treatment). If you are looking for detailed guidance on what to prepare, why, and how, I highly recommend the book The Art of Dying Well: A Practical Guide to a Good End of Life by Katy Butler. The book goes into great detail things to consider and how best to ensure wishes are followed using the various legal options available.

Streamlining Caregiving. To combat the feeling of being "pressed for time," caregivers can leverage technology and organization to streamline their responsibilities. This can include automating as many tasks as possible, such as prescription and grocery deliveries, and using caregiving apps or a simple notebook to keep all important information organized in one place.

Caring for the Caregiver: Avoiding Burnout

The emotional strain of caregiving can be significant, and it is a mistake to ignore the signs of burnout.

Recognizing the Signs. The psychological toll of caregiving can manifest in increased stress, sadness, anxiety, and an elevated risk for stress-related illnesses. Burnout symptoms can include feeling emotionally fragile, withdrawing from friends and family, and using unhealthy coping mechanisms such as drugs and alcohol. The feeling of guilt, that one is not doing enough or is a "bad caregiver" for needing a break, is a particularly harmful emotion that can lead to depression and anxiety.

The Case for Self-Care. Self-care is not a luxury; it is a necessity for a caregiver's physical and mental health. Taking time for activities that strengthen you both physically and emotionally, such as regular exercise, a walk, or simply reading a book, can help prevent burnout and provide the mental fortitude needed to manage the challenges of caregiving.

Finding Your Support System. Finally, no one should attempt to navigate this journey alone. It is important to establish a strong support system, which can include professional help and peer support. Joining a caregiver support group or engaging a therapist, either in person or online, can provide immense relief by connecting individuals with others who understand their situation.

Conclusion: A Proactive Path Forward

The challenges facing the sandwich generation are complex, deeply personal, and here to stay. While the financial pressures are real and significant, they can be managed with a strategic and empathetic approach. The most successful path forward begins with a foundation of personal financial security.

By prioritizing your own retirement, you empower yourself to be a source of strength for your entire family and not be a burden to your children. This foundation then allows you to address the needs of your children and parents, whether through education savings plans, support, financial means, or by leveraging government resources. At Purpose Built, we help you create and implement a financial blueprint that coordinates goals across all three generations, ensuring you have the resources and peace of mind to secure everyone's future.

Let’s talk and build your Sandwich Generation playbook.

FAQ (Frequently Asked Questions)

Q: What is the "Sandwich Generation," and why are high-earning households particularly affected?

A: The "Sandwich Generation" refers to adults supporting both their aging parents and their own children. High-earning households are impacted by the compounded financial stress of rising elder care costs and the high cost of raising a child, which can jeopardize their personal retirement savings and professional trajectories.

Q: What are the key financial steps I should take to prepare for this challenge?

A: Begin by solidifying your own financial foundation. Maximize retirement contributions, build a robust emergency fund, and use tax-advantaged accounts like a 401(k) and HSA. Then, create a strategic plan for your children's education and your parents' long-term care.

Q: Should I use a 529 plan or a custodial account for my child’s education?

A: For high-earning families, a 529 plan is generally recommended. It offers tax-advantaged growth and a lower impact on financial aid eligibility compared to a custodial account, where funds are legally owned by the child and can affect their eligibility.

Q: How do I talk to my parents about their finances without causing family conflict?

A: Approach the conversation with empathy and respect. Frame the discussion around honoring their wishes and ensuring their well-being, not about controlling their finances. Consider hiring a neutral third party, like a financial planner, to facilitate the conversation.

Q: What is Purpose Built's role in helping the Sandwich Generation?

A: Purpose Built specializes in creating comprehensive financial blueprints that coordinate the goals of all three generations. We help you implement strategies to manage your parents' care, secure your children's future, and safeguard your own retirement, all while minimizing stress and maximizing financial stability.

Final thoughts

You don’t need to choose between your parents, your kids, and your own future; you need a plan. Start with your plan (oxygen mask), put structure around how you help (cash-flow caps, written agreements), and squeeze every available tax lever. The result is a calmer household, less financial drag, and a higher probability that everyone gets where they’re going.

If you want help turning this into a concrete, multi-year plan including cash-flow maps, tax modeling, and “who-pays-what-when” rules you can actually live with, Purpose Built does this all day. We’ll build your numbers, coordinate estate attorneys, reduce the number of professionals needed since we also prepare your personal income taxes, and give you a playbook you can run with confidence.

Let’s talk. We’ll help you support the people you love and protect the future you’re building.

About the Author

Sean Lovison, CPA, CFP®, is a fee-only financial planner based in Moorestown, New Jersey, serving clients virtually nationwide. After spending 14 years as a corporate chief financial officer (CFO), receiving and designing compensation plans, he decided to help others navigate their plans.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Sean Lovison and Purpose Built Financial Services (PBFS), unless otherwise specifically cited. The material presented is believed to be from reliable sources, and no representations are made by our firm regarding other parties' informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant, or legal counsel prior to implementation.

The information on this site is provided "AS IS" and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, PBFS disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. PBFS does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall PB be liable for any direct, indirect, special, or consequential damages that result from the use of, or the inability to use, the materials on this site, even if PB or a PB-authorized representative has been advised of the possibility of such damages. In no event shall Purpose Built have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

.jpg)