5 Key Takeaways: Planning for Your Longer Retirement

- Life Expectancy Misconception: Average life expectancy "at birth" dramatically underestimates longevity for those who reach age 65; plan for a retirement extending well into your mid-80s or beyond.

- Maximize Social Security: Delaying Social Security until age 70 significantly boosts your guaranteed, inflation-adjusted income for life, a strategy heavily favored by extended longevity.

- Unlock Roth Advantage: Roth conversions eliminate future RMDs and provide decades of tax-free growth and withdrawals, critically valuable for a longer retirement and managing future tax burdens.

- Mitigate Widow(er) Penalty: Strategic Roth conversions reduce RMDs, helping surviving spouses avoid punitive higher tax brackets when shifting to single filing status after their spouse's passing.

- Advisor's Role is Crucial: A trusted financial advisor serves as an educator and confidant, countering emotional biases with data and optimizing complex strategies for your true longevity and peace of mind.

For high-achieving professionals and executives, retirement planning is a constant exercise in balancing current goals with future needs. You meticulously manage investments, scrutinize tax strategies, and project cash flows. Yet, when it comes to two of the most powerful strategies for maximizing lifetime wealth, delaying Social Security and executing Roth conversions, a common, often by males, objection frequently arises: "I won't live long enough for that to make sense."

This sentiment, while understandable, is often rooted in a misinterpretation of life expectancy data and can lead to leaving hundreds of thousands, if not millions, of dollars on the table over the course of a long retirement. For those who reach their retirement years, a significantly longer lifespan is a more realistic expectation, impacting the value of these strategic decisions.

We'll also discuss at a high-level delaying Social Security and leveraging Roth conversions and how these planning tools can build a more secure, tax-efficient, and stress-free retirement, far outweighing the perceived "payback period" when viewed through the lens of accurate longevity projections. We don’t dig into either option in too much detail as individual, more thorough articles are needed to discuss them.

The Life Expectancy Fallacy: Why Averages Can Mislead

When people say, "I won't live long enough," they often cite the average life expectancy for a person at birth (if they cite anything other than their gut feeling!). For instance, the most recent data released by the National Center for Health Statistics in December 2024 for the general U.S. population shows an average life expectancy around 77-78 years for both sexes.

They will then argue that waiting until age 70 to collect social security only to die 7 years later is not a good return, they could do better by collecting early and investing the difference. Calculating a breakeven between collecting and investing requires an investment return assumption which is always an estimate but AARP calculated the breakeven to be just under 79. If you read that study, then look at the average mortality rate above of ~78, then it certainly does not make sense to wait to collect.

However, while this figure is accurate for a newborn, it dramatically underestimates the outlook for someone who has already reached their 60s.

The average life expectancy at birth accounts for all causes of mortality throughout a lifetime, including infant mortality, accidents in early adulthood, and illnesses in middle age. If you've already navigated these earlier life stages and made it to retirement age, your statistical probability of living much longer than the "at birth" average increases significantly. You come “from good stock” to use a hotly debated analogy (Does the saying “good stock” come from agricultural breeding or come the genealogical, more literal meaning of a tree trunk or stump to denote the lineage of your family tree?).

Let's look at the data to understand this crucial difference:

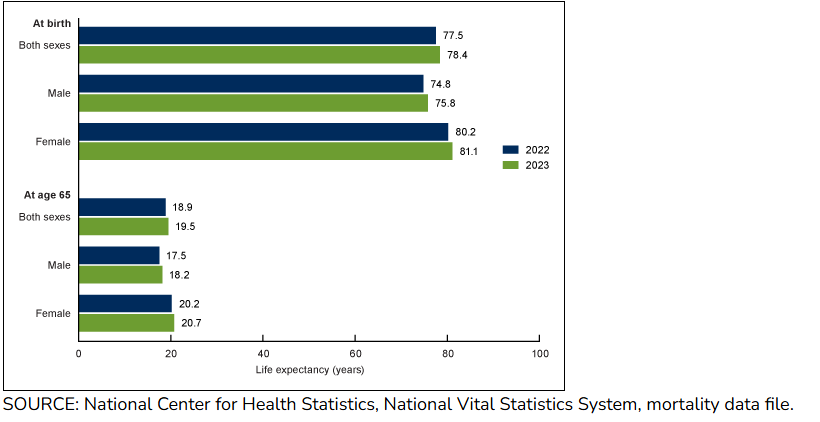

Life Expectancy in the U.S.: At Birth vs. At Age 65

This data clearly illustrates the point:

- While a male born in 2023 had a life expectancy of roughly 78.8 years, a male who reaches age 65 in 2023 can expect to live an additional 18.2 years, putting his total expected lifespan at 83.2 years.

- For females, the difference is even more pronounced. A female born in 2023 had a life expectancy of 81.1 years, but if she reaches age 65, she can expect to live an additional 20.7 years, bringing her total expected lifespan to 85.7 years.

- For both sexes combined, reaching age 65 means an additional 19.5 years of life expectancy, pushing the average expected lifespan well into the mid-80s.

These numbers are averages, meaning many will live even longer. For healthy, affluent professionals with access to quality healthcare and active lifestyles, living well into their late 80s or even 90s is increasingly common. This extended longevity fundamentally changes the math for retirement strategies.

If you want to check out the statistics for your exact age and situation, the Social Security created this cool tool to see how long the data says you will probably live: Retirement & Survivors Benefits: Life Expectancy Calculator

The Power of Delaying Social Security

One of the most impactful decisions in retirement planning is when to claim Social Security benefits. While some may claim as early as age 62, the strategy of delaying benefits can lead to a significantly higher guaranteed income stream for the rest of your life.

How Delaying Works:

Your Social Security benefit increases by a certain percentage for each year you delay claiming, past your Full Retirement Age (FRA), up to age 70. These are called Delayed Retirement Credits (DRCs).

- If your FRA is 67, delaying until age 70 can increase your monthly benefit by approximately 24% compared to what you would receive at FRA. This increase is permanent, inflation-adjusted, and guaranteed by the U.S. government.

How Taking Early Works:

Taking social security earlier than your full retirement age (67 for most people) is possible, you may take it as early as 62 however it works the opposite as our delaying calculation above.

- Claiming at age 62 reduces your monthly benefit by approximately 6% for each year you claim before your full retirement age. For those born in 1960 or later, the full retirement age is 67, which means claiming at 62 (five years early) results in a 30% reduction. That reduction is forever.

However, as previously mentioned in the opening, some individuals believe they can collect early, invest the funds themselves, and ultimately come out ahead. This perspective largely stems from the belief that they will not live much beyond 70 to benefit from the significant increase gained by delaying collection.

Why Longevity Makes it a "No-Brainer":

This argument against delaying is based on trying to find the "breakeven point" - the age at which the cumulative higher payments from delaying overtake the cumulative payments from claiming early. A breakeven analysis is highly subjective since a return assumption needs to be made but we know that AARP estimated it to be 79 years old.

Now incorporating the actual numbers from the National Health Center, that the average 65-year-old can expect to live into their mid-80s, delaying Social Security ensures that you are very likely to not only reach, but significantly surpass, that break-even point. This means you will receive a higher guaranteed income for many years when you may need it most, particularly for late-life healthcare costs or maintaining your lifestyle.

This strategy effectively provides you with a higher, inflation-adjusted annuity, paid for by your earlier contributions. It's often one of the best "investments" you can make to hedge longevity risk, the risk that you may outlive your assets because you live longer than you assumed.

Future-Proofing Wealth: The Strategic Advantage of Roth Conversions

Another powerful strategy often overlooked or delayed due to the "I won't live long enough" mindset is the Roth conversion. Many high-income professionals accumulate substantial pre-tax assets in 401(k)s and IRAs, postponing taxes until retirement. While logical for tax deferral, this can create a ticking tax time bomb later in life.

How Roth Conversions Work:

A Roth conversion involves taking pre-tax money from a traditional IRA or 401(k) and moving it into a Roth IRA. You pay income tax on the converted amount in the year of conversion. The benefit: all future growth on that money is tax-free, and qualified withdrawals in retirement are completely tax-free.

They are especially powerful for high earners who often have the desire and financial means to retire early, creating a period of low tax earnings before social security starts (hopefully at 70 like we outlined above) and RMDs kick in. This period is the peak tax planning window and should be filled with Roth Conversions.

Why Longevity Makes Them Essential:

For someone expecting to live into their mid-80s or beyond, a Roth conversion becomes incredibly appealing for several reasons:

- Tax-Free Growth for Decades: Every year that money grows tax-free in a Roth account is immensely powerful. An extra 5-10 years of tax-free compounding can make a monumental difference in your total wealth.

- Tax-Free Withdrawals in Retirement: Imagine withdrawing $50,000, $100,000, or more per year from your Roth account in your 80s and 90s, knowing that every dollar is yours, free from federal and state income taxes and potential tax rate increases. This is a game-changer for managing your retirement income and minimizing your overall tax burden.

- Required Minimum Distributions (RMDs): Unlike traditional IRAs, Roth IRAs do not have RMDs during the original owner's lifetime. This gives you ultimate control over when you take distributions, allowing your money to continue growing tax-free for as long as possible. For those facing high RMDs in their 70s and 80s, Roth conversions can significantly reduce future taxable income.

- Widow(er) Penalty: One benefit of Roth conversions, often overlooked due to its sensitive nature, is its potential to help avoid the Widow(er) Penalty created by RMDs. The sad fact is, we don't all live the life portrayed in The Notebook where both spouses pass together.

More commonly, when one spouse dies, the survivor typically gets a two-year tax break (plus the year of passing) filing as a Qualifying Surviving Spouse (QSS), maintaining favorable Married Filing Jointly (MFJ) rates. After this period, they usually file as single, facing significantly higher tax brackets for the same income. The problem? Their RMDs and total assets often remain the same. This can lead to a substantial "Widow(er) Penalty," pushing them into higher tax brackets.

Roth conversions proactively help by reducing future RMDs before this situation occurs. By shifting pre-tax dollars into Roth accounts during both spouses' lifetimes, you shrink the traditional IRA balance subject to RMDs, lowering the surviving spouse's future taxable income and mitigating this painful tax increase.

- Legacy Planning: Roth accounts can be excellent for heirs, as they receive the assets tax-free (with certain distribution rules), offering a powerful tax-advantaged inheritance. This contrasts with pre-tax retirement plans, such as Traditional IRA and 401(k)s, which pass to their beneficiaries who then often have a limited amount of time to withdraw all the funds (usually 10 years). This can create quite the tax hit to the legacy you were hoping to leave to your children since they are often at their highest earning years and therefore tax rates.

The "payback period" for Roth conversions isn't about dying earlier, but about how long your money will grow tax-free and how long you'll benefit from tax-free income in retirement. With an expected lifespan well into the 80s, that "payback" is often a lifetime of tax advantages.

The Advisor's Role: Education, Clarity, and Peace of Mind

The decision to delay Social Security or execute Roth conversions involves complex calculations, tax implications, and a deep understanding of your personal financial situation and goals. This is where a relationship with a trusted financial advisor becomes indispensable.

Many high-income professionals are incredibly intelligent but are still susceptible to common cognitive biases, especially when it comes to long-term financial decisions. The "I won't live long enough" argument is often less about statistics and more about an underlying anxiety about the future, a desire for immediate gratification, or a fear of making the "wrong" decision.

At Purpose Built, we understand that financial planning isn't just about numbers; it's about people. Our role extends beyond mere calculations; it often involves acting as a trusted confidant, almost like a "financial therapist," to help you:

- Educate with Facts: We present the real data on longevity, break-even points, and tax impacts, providing clear, unbiased information to counter common misconceptions and emotional biases.

- Ease Anxiety: We create comprehensive financial plans that model different scenarios, illustrating how delaying Social Security and executing Roth conversions can lead to a more secure, flexible, and tax-efficient retirement, alleviating the fear of the unknown.

- Optimize for Your Life: We tailor these strategies to your unique health, family situation, income needs, and legacy goals. We consider your overall tax picture, cash flow, and other assets to determine the optimal timing and amount for Roth conversions.

- Provide Control and Confidence: By proactively planning, we give you greater control over your future income streams and tax liabilities. This structured approach replaces uncertainty with confidence, allowing you to focus on enjoying your hard-earned success.

Plan for the Life You've Earned

You've worked hard to build substantial wealth and a successful career. Don't let a common misconception about life expectancy diminish your retirement. The data overwhelmingly suggests that if you've made it to age 60 or 65, you have many, many vibrant years ahead.

Embracing strategies like delaying Social Security and executing well-timed Roth conversions isn't about gambling on longevity; it's about strategically maximizing the value of your assets over a statistically probable long and active retirement while creating confidence in your financial security. These are not just technical maneuvers; they are powerful tools that unlock greater financial security, tax efficiency, and, ultimately, more peace of mind.

Don't leave significant value on the table due to an outdated perspective. Contact Purpose Built today to discover how our comprehensive financial planning can help you align your strategies with your true longevity, ensuring your retirement is as prosperous and fulfilling as you deserve.

Frequently Asked Questions (FAQ)

Q: Why is citing average life expectancy "at birth" misleading for retirement planning?

A: Life expectancy "at birth" includes all mortality risks from infancy through adulthood. For someone who has already reached age 60 or 65, their actual statistical life expectancy is significantly longer, often well into their mid-80s, making long-term strategies more impactful.

Q: How does delaying Social Security until age 70 benefit someone likely to live into their mid-80s?

A: Delaying Social Security provides permanent, inflation-adjusted increases to your monthly benefit. For a 65-year-old expecting to live into their mid-80s, you will likely surpass the "break-even point" and receive a higher guaranteed income for many years, covering late-life expenses.

Q: What are the primary benefits of Roth conversions for a long retirement?

A: Roth conversions offer tax-free growth for decades and tax-free withdrawals in retirement, eliminating future RMDs during your lifetime. This provides significant control over your retirement income, minimizes future tax liabilities, and builds a powerful tax-advantaged legacy.

Q: What is the "Widow(er) Penalty" and how can Roth conversions help?

A: The Widow(er) Penalty refers to a surviving spouse moving into higher single tax brackets while their RMDs and assets often remain the same after a spouse's passing. Roth conversions reduce future RMDs from pre-tax accounts, mitigating this tax increase and protecting the survivor's financial security.

Q: How can a financial advisor help me with these complex longevity-based strategies?

A: A trusted financial advisor provides objective education, models personalized scenarios, and helps you overcome emotional biases. They optimize strategies like Social Security delay and Roth conversions to fit your unique situation, giving you greater control, confidence, and peace of mind for a long retirement.

Final Thoughts: Plan for the Prosperity You Deserve

You've worked hard to build substantial wealth and a successful career. Don't let a common misconception about life expectancy diminish your retirement. The data overwhelmingly suggests that if you've made it to age 60 or 65, you have many, many vibrant years ahead.

Embracing strategies like delaying Social Security and executing well-timed Roth conversions isn't about gambling on longevity; it's about strategically maximizing the value of your assets over a statistically probable long and active retirement while creating confidence in your financial security. These are not just technical maneuvers; they are powerful tools that unlock greater financial security, tax efficiency, and, ultimately, more peace of mind.

Don't leave significant value on the table due to an outdated perspective. Contact Purpose Built today to discover how our comprehensive financial planning can help you align your strategies with your true longevity, ensuring your retirement is as prosperous and fulfilling as you deserve.

About the Author

Sean Lovison, CPA, CFP®, is a fee-only financial planner serving clients virtually nationwide but based in Moorestown, New Jersey. After spending 14 years as a corporate chief financial officer (CFO), receiving and designing compensation plans, he decided to help others navigate their plans.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Sean Lovison and Purpose Built Financial Services (PBFS), unless otherwise specifically cited. The material presented is believed to be from reliable sources, and no representations are made by our firm regarding other parties' informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant, or legal counsel prior to implementation.

The information on this site is provided "AS IS" and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, PBFS disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. PBFS does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall PB be liable for any direct, indirect, special, or consequential damages that result from the use of, or the inability to use, the materials on this site, even if PB or a PB-authorized representative has been advised of the possibility of such damages. In no event shall Purpose Built have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

.jpg)